By Brian Kowalski November 7, 2025

Comparing credit card processing rates in Erie, Pennsylvania can feel complicated, but the process becomes manageable when you know what to look for and how to calculate your true costs.

This guide explains every element that shapes your effective rate, how regional dynamics affect fees, and the exact steps to audit statements, negotiate with providers, and future‑proof your setup.

You’ll learn how interchange, assessments, and processor markups work together; what equipment and gateways really cost over time; and how local Erie business patterns—lake‑effect seasonality, tourism, and university traffic—change your risk and pricing profile.

Use the checklists, formulas, and negotiation scripts here to compare apples to apples and lock in fair, transparent pricing for your business in Erie, Pennsylvania.

Why comparing credit card processing rates in Erie, Pennsylvania matters

When you compare credit card processing rates in Erie, Pennsylvania methodically, you protect margins without sacrificing customer experience. Many merchants focus on a headline “discount rate,” but that single figure hides multiple moving parts that add up to the number that really matters: your effective rate.

Erie’s economy includes restaurants, retail, healthcare, trades, professional services, and seasonal tourism tied to Presque Isle and Lake Erie. Each segment runs different average tickets, fraud exposure, and card mix, which change costs dramatically.

A coffee shop with high volume and low tickets is sensitive to per‑transaction fees. A contractor or marina with higher tickets feels interchange and chargeback risk more. If you don’t compare offers line by line—interchange category, assessments, processor markup, monthly fees, PCI, gateway, POS, and contract terms—you can end up overpaying without realizing it.

A careful comparison also surfaces hidden fees and equipment leases that quietly inflate your total cost of ownership. In short, a smart comparison turns processing from a sunk cost into a controllable expense—crucial for Erie businesses competing on thin margins.

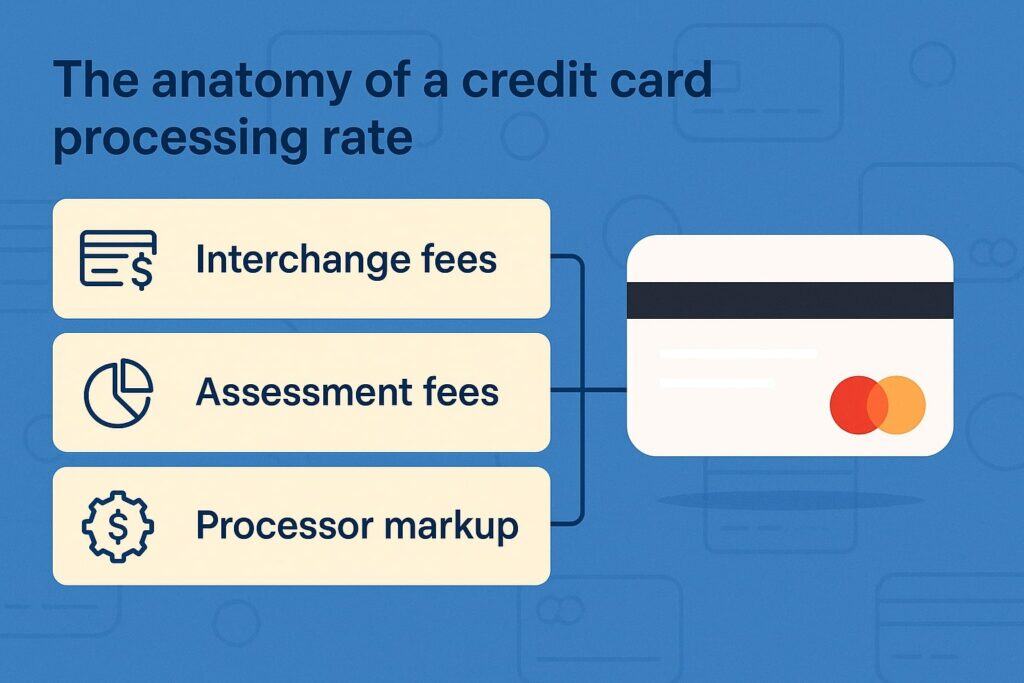

The anatomy of a credit card processing rate

Every quote for credit card processing rates in Erie, Pennsylvania has three layers: interchange, assessments, and processor markup. Interchange is set by the card brands and paid to issuing banks; it varies by card type, transaction method, and industry.

Assessments are network fees set by the brands on top of interchange. Processor markup is what your payment processor earns to support you—statementing, risk monitoring, customer service, gateways, and hardware.

When you compare offers, separate these layers. Interchange and assessments are largely non‑negotiable and the same for every processor; markup is negotiable. If one offer “includes interchange,” be cautious: it may be a blended or tiered plan that obscures true costs.

For a clean comparison, request interchange‑plus or membership/pricing with published margins. Ask for the per‑transaction fee, the percentage markup, and all monthly costs in writing.

Confirm how card‑present versus card‑not‑present transactions are priced, what the gateway adds, and how BNPL, AMEX, and digital wallets are handled. Knowing the anatomy ensures you compare the same components across providers.

Interchange

Interchange is the wholesale cost of moving money from your customer’s issuing bank to your Erie, Pennsylvania business. It depends on the card brand (Visa, Mastercard, Amex, Discover), card type (debit, credit, rewards, commercial), entry method (EMV, contactless, keyed, e‑commerce), and data quality (address verification, Level II/III).

Card‑present EMV transactions with debit often price best. Keyed or ecommerce transactions cost more due to higher risk. Interchange is published in complex tables, but you don’t need to memorize them to compare offers.

What you need is clarity on your card mix and average ticket so you can estimate how many transactions will fall into common categories.

For example, a quick‑service restaurant will see many regulated and unregulated debit transactions with low tickets; a B2B distributor might qualify for Level II/III interchange optimization if it sends enhanced data.

When you compare credit card processing rates in Erie, Pennsylvania, ask each provider to map your last three months of sales into projected interchange categories so you can see how their markup sits on top of real, expected costs.

Assessments and network costs

Assessments are network‑level fees from the card brands. They’re separate from interchange and are typically small percentages or per‑item charges applied to volume. Examples include brand assessments, network access fees, and cross‑border or card‑brand specific add‑ons.

Assessments are generally non‑negotiable and identical regardless of your processor. When evaluating credit card processing rates in Erie, Pennsylvania, make sure assessments are not being marked up or “blended” in ways that hide them inside a tiered rate.

A transparent statement lists assessments separately by brand so you can reconcile them to public schedules. While assessments may seem minor, they add up—especially if your card mix includes premium rewards or international cards from tourism tied to Presque Isle State Park visitors.

Confirm how digital wallets (Apple Pay, Google Pay), contactless, and “guest checkout” transactions are classified, and whether any additional network or tokenization fees appear. Properly itemized assessments make your apples‑to‑apples comparison much more accurate.

Processor markup models explained

Processors use several markup models: flat‑rate/blended, tiered (qualified/mid/non‑qualified), interchange‑plus, and membership/subscription pricing. Flat‑rate quotes look simple, but they make it hard to validate true costs; you may pay more on low‑cost debit and less on premium rewards, averaging out to a convenience tax.

Tiered pricing is common but can hide reclassification risk: more transactions “downgrade” into expensive tiers over time. Interchange‑plus is the most transparent: you pay actual interchange and assessments plus a fixed markup (for example, +0.15% and $0.08).

Membership/subscription models charge a monthly fee and pass through interchange and assessments with minimal per‑transaction markup, which can be advantageous for higher‑volume Erie merchants.

When comparing credit card processing rates in Erie, Pennsylvania, ask each provider to present interchange‑plus or membership pricing, list every fixed fee, and include a sample effective‑rate calculation based on your actual statement data. The right model depends on your mix, but transparency always helps you win.

Erie, Pennsylvania specifics that affect pricing

Local dynamics influence credit card processing rates in Erie, Pennsylvania. Lake‑effect weather and tourism create seasonal swings that change volume, average ticket, and chargeback risk.

Universities like Penn State Behrend and nearby colleges bring student cardholders with strong debit usage during semesters, then dip in summer. Healthcare, trades, and marinas see larger tickets and more card‑not‑present invoices, which alter interchange categories.

Erie’s small‑business ecosystem also favors point‑of‑sale systems with offline‑capable EMV for winter storms and reliable broadband failover.

Ask processors how they handle seasonality: do they offer month‑to‑month contracts, seasonal holds, or minimum fee waivers in slow months? Clarify Pennsylvania rules around surcharging and cash discounting, signage, and receipt disclosures.

Finally, Erie’s proximity to Ohio and New York can introduce cross‑border card usage from travelers; verify how your provider classifies those transactions and whether any international assessment applies.

A provider that understands Erie’s rhythms will forecast your effective rate more accurately and help you keep costs predictable all year.

Card‑present vs. card‑not‑present in Erie

Card‑present transactions (EMV chip and contactless) usually price better than card‑not‑present (keyed, phone, e‑commerce) because they carry less fraud risk.

Many Erie merchants straddle both worlds: a boutique that sells in‑ stores and ships online, a restaurant running dine‑in plus online orders, or a contractor taking deposits in person and progress payments by invoice.

When comparing credit card processing rates in Erie, Pennsylvania, request separate pricing for card‑present and card‑not‑present, including gateway and tokenization fees for the online channel.

Confirm whether your POS supports EMV fallback rules, tip adjustment for hospitality, and offline mode for storm‑related outages. For e‑commerce, check for 3‑D Secure support, address verification, and fraud scoring.

Small per‑transaction gateway fees can outweigh percentage markups on low tickets, so include them in your effective‑rate math. If you plan to offer to buy‑now‑pay‑later or text‑to‑pay, verify how those rails price and settle. Aligning your acceptance methods to Erie’s shopping patterns reduces your blended cost.

How to calculate your effective rate step by step

Your effective rate is total processing cost divided by total processed volume in a period. It’s the only metric that converts the maze of line items into one comparable number.

To calculate it, pull one month of statements and add: interchange, assessments, processor percentage markup, per‑transaction fees, monthly fees (statement, PCI, gateway), chargeback fees, POS SaaS fees, and any network access or tokenization fees.

Divide by the gross card volume for that month. Do this for three consecutive months to smooth out seasonal spikes common in Erie, Pennsylvania. When comparing credit card processing rates in Erie, Pennsylvania, ask each provider to price your last three months of data using the same method.

Request a spreadsheet that shows per‑line assumptions: average ticket, transaction count, card mix, and keyed percentage. If a provider refuses, treat that as a red flag.

Once you know your effective rate today, you can quantify savings from a new offer and weigh them against switching costs like hardware, training, or contract termination.

Sample Erie merchant scenarios

Consider three simplified scenarios to compare credit card processing rates in Erie, Pennsylvania. A quick‑service café runs $35,000/month with a $9 average ticket and 70% debit, all card‑present. The café’s sensitivity is per‑transaction fees; shaving $0.03 per swipe may beat a 0.05% percentage cut.

A lakeside retailer processes $80,000/month with a $45 average ticket, a mix of rewards credit, and seasonal peaks. For them, an interchange‑plus plan with low per‑item fees and month‑to‑month terms fits volatility.

A contractor invoices $120,000/month with a $900 average ticket, 60% card‑not‑present. They benefit from address verification, 3‑D Secure, and Level II data to optimize interchange. In each scenario, compute effective rate by including gateway costs, PCI fees, and any chargebacks.

Run a three‑month projection reflecting Erie’s seasonality and tourism. Using this structured approach, you will see that the best quote isn’t always the one with the lowest headline rate—it’s the one that lowers your effective rate once all Erie‑specific realities are priced in.

Statement audit checklist for Erie merchants

A disciplined statement audit is the fastest way to compare credit card processing rates in Erie, Pennsylvania. First, pull three months of detailed statements and export any available data to CSV.

Second, group charges into: interchange, assessments, percentage markup, per‑transaction fees, monthly fees, PCI, gateway, POS subscription, chargeback and retrieval fees, and equipment or lease charges.

Third, verify card‑present versus card‑not‑present counts and the percentage of keyed entries. Fourth, spot “downgrades” where transactions are priced in higher categories due to missing data or tip adjustment delays—common in hospitality.

Fifth, reconcile assessments to brand schedules and confirm none are inflated. Sixth, review contract items: monthly minimums, statement fees, PCI non‑compliance fees, batch fees, and annual fees. Seventh, compute the effective rate for each month and average them.

Finally, use your audit to request an interchange‑plus or membership quote where every markup component is explicit. This process turns subjective sales claims into objective numbers you can compare.

Hidden fees to watch (and how to spot them)

When you compare credit card processing rates in Erie, Pennsylvania, hidden fees can distort your decision. Look for PCI “non‑completion” charges even when you validated compliance, statement “delivery” fees despite e‑statements, and inflated “network” or “regulatory” surcharges that duplicate assessments.

Watch for excessive batch fees, AVS fees on card‑present transactions, or gateway “token” charges for the same transaction twice. Scrutinize address‑verification and 3‑D Secure fees; they can be worth it for fraud control, but they must be counted in your effective‑rate math.

If a provider quotes a super‑low percent but adds $25–$40 in monthly SaaS and multiple $5–$10 line items, the true cost may be higher than a cleaner interchange‑plus offer. Demand a one‑page schedule of fees that lists every possible charge.

Ask whether fees are flat, tiered by volume, or subject to “program changes.” A transparent provider will explain each fee’s purpose and help you eliminate those you don’t need.

Hardware, gateways, and POS: pricing and fit

Your equipment and software stack drive both cost and usability. For card‑present sales in Erie, Pennsylvania, choose EMV‑capable terminals that also support contactless and PIN debit. Confirm whether devices are sold, rented, or leased—avoid long‑term non‑cancelable leases, which can lock you into high costs.

For POS, compare total monthly SaaS, app add‑ons, and payment gateway fees. In omnichannel setups, ensure your gateway supports tokenization, vaulted cards, and unified reporting so in‑store and online data roll up cleanly.

Ask about offline mode for winter weather outages and cellular failover. If you serve marinas or outdoor venues, consider ruggedized devices and splash resistance. For e‑commerce, check cart integrations, subscription billing, invoice links, and text‑to‑pay.

Include the cost of readers, chargers, stands, and replacement units in your total cost of ownership. Most importantly, price how each hardware/gateway choice affects your effective rate by changing per‑item fees and available optimization tools.

Surcharging, cash discounting, and dual pricing in Pennsylvania

Legal and card‑brand rules for passing fees to customers vary by state and evolve. In Pennsylvania, you must follow brand rules on surcharging, signage, disclosure, and caps if you choose to surcharge credit transactions.

Debit and prepaid cards cannot be surcharged. Cash discounting and dual pricing programs require clear posted pricing and must not misrepresent the “regular” price. When comparing credit card processing rates in Erie, Pennsylvania, ask providers for written compliance guidance, sample signage, and POS configuration support.

Ensure your receipts display both the base price and any service fee. Train staff to handle customer questions and to remove fees when prohibited (for example, on debit routed as PIN).

Even if you decide not to surcharge, dual pricing can nudge cash usage in certain sectors, but weigh the potential customer impact. The safest path is transparent pricing that complies with card‑brand rules and Pennsylvania consumer‑protection standards, backed by a provider willing to put its guidance in writing.

Negotiation playbook for better pricing

Approach negotiations armed with data. Use your statement audit to calculate current effective rate and identify cost drivers. Request written quotes for interchange‑plus or membership pricing that specify percentage markup, per‑transaction fees, and all monthly charges.

Ask for month‑to‑month terms, no liquidated‑damages early termination, and no non‑cancelable equipment leases. Seek gateway fee caps or volume‑based discounts. If you’re seasonal, negotiate minimum‑fee waivers for slow months common in Erie, Pennsylvania.

Benchmark with at least two competing offers using the same three months of your real data. Push for service‑level commitments: dispute response times, dedicated support contacts, and hardware replacement SLAs during winter peaks.

Finally, insist on a “no hidden fees” addendum that prohibits new line items without your written approval. This process reframes the conversation from “What’s your rate?” to “Here’s my cost structure—match or beat it transparently.”

Contract terms to scrutinize

Contracts can erase savings if they contain traps. When comparing credit card processing rates in Erie, Pennsylvania, read for early termination language (liquidated damages, auto‑renewal), monthly minimums that punish seasonality, and statement or PCI fees that stack up.

Look for equipment leases that run 36–60 months with personal guarantees—these are costly and hard to exit. Confirm the term for gateway or POS SaaS and whether price increases are capped.

Check if your processor can raise markup with “program changes” clauses. Verify who owns your terminal keys and whether devices are processor‑locked, which complicates switching. Note chargeback and retrieval fees, representation costs, and any “pre‑arbitration” charges.

Ask for a single, consolidated schedule of fees that overrides conflicting marketing materials. Before signing, send a redlined copy that removes penalties, secures month‑to‑month terms, and clarifies ownership of hardware. Strong terms lock in savings beyond the headline rate.

Security, PCI, and fraud tools that lower cost

Fraud and PCI issues quietly raise your effective rate through chargebacks, higher interchange categories, and non‑compliance fees. To compare credit card processing rates in Erie, Pennsylvania properly, include the cost and benefit of security tools.

Aim for EMV, contactless, point‑to‑point encryption (P2PE), and tokenization across channels. For ecommerce or mail/phone orders, enable address verification (AVS), CVV checks, velocity limits, and 3‑D Secure where appropriate.

Consider Level II/III data for B2B to qualify for better interchange. Make PCI validation easy: a guided portal, quarterly scans if needed, and clear remediation steps.

Ask providers how they monitor for friendly fraud, how quickly they notify you about disputes, and whether they offer automatic evidence packs for representation. Preventing a handful of disputes each month or downgrades due to missing data can save more than shaving a few basis points off markup.

Chargeback management and representment

Chargebacks cost fees, labor, and potential increases in monitoring program risk. Build a dispute playbook as part of comparing credit card processing rates in Erie, Pennsylvania. Capture clear receipts, delivery proofs, and signed work orders.

Use descriptor clarity so customers in Erie recognize your business name on statements. Enable alerts for pending disputes so you can refund strategically before a formal chargeback.

For hospitality and retail, train staff on tip adjustments and EMV fallback to prevent no‑signature or fallback downgrades. Ask providers about integrated tools that auto‑gather evidence—AVS results, delivery tracking, and signed invoices—into a representation package.

Measure your win rate and reasons for losses, then fix root causes such as unclear refund policies or recurring billing confusion. Reducing your dispute rate keeps you out of network monitoring programs and preserves lower pricing tiers.

Online vs. in‑store strategies for Erie merchants

Your blended cost depends on where and how you take cards. In‑store EMV with contactless is efficient and fast for Erie’s busy seasons. Online expands reach during storms and off‑season months but adds gateway and fraud‑tool costs.

To compare credit card processing rates in Erie, Pennsylvania, model two channels separately, then blend them with your expected volume split. For restaurants, confirm online ordering and tip flows, saved cards, and QR pay.

For boutiques, evaluate buy‑online‑pickup‑in‑store with a single customer profile to avoid duplicate token fees. For trades and healthcare, use invoice links and recurring billing with 3‑D Secure on higher‑risk transactions.

Always include the cost of features you’ll actually use, not a longer list of addons you won’t. The best plan is the one that aligns to your Erie customers’ habits while keeping your data unified and secure.

Omnichannel reporting and tokenization benefits

Omnichannel tokenization lets a customer pay in your store, on your site, or by invoice using the same vaulted card, while your system tracks them as one profile. This raises conversion and simplifies reporting, but it can introduce token or vault fees.

When comparing credit card processing rates in Erie, Pennsylvania, check whether your provider charges per‑token, per‑vaulted card, or per‑transaction tokenization fees, and whether those fees duplicate gateway charges.

A unified token reduces chargebacks by allowing you to recognize returning customers and apply consistent fraud rules. It also supports seamless customer experiences—on‑file for deposits, contactless on site, and one‑click online.

Price these benefits into your effective‑rate math by modeling higher approval rates and lower chargebacks. The right omnichannel setup often saves money even if nominal gateway fees look higher on paper.

Total cost of ownership and forecasting

Effective comparisons look beyond this month’s statement. Build a 12‑month forecast to compare credit card processing rates in Erie, Pennsylvania by modeling expected volume, average ticket, card mix, and channel split for each month.

Add subscription costs for POS, gateway, and apps. Include hardware depreciation or replacement. Factor in seasonality from Presque Isle tourism, university calendars, and winter storms. Model chargebacks, dispute fees, and any interchange optimization improvements you plan, such as Level II/III data for B2B.

Finally, include one‑time costs to switch: contract termination, hardware purchases, or staff training. With a forecast, you’ll see whether a subscription/membership model outperforms interchange‑plus, or whether a slightly higher per‑item fee is offset by lower SaaS. Forecasting turns your choice into a business plan rather than a bet on a teaser headline rate.

KPIs and a quarterly review cadence

Set payment KPIs so you know whether your decision works. For Erie, Pennsylvania businesses, track effective rate, approval rate, chargeback ratio, downgrade/downgrade rate, and average authorization time for busy weekends and weather events.

Review your performance quarterly, not yearly; Erie’s seasonality can hide trends if you wait too long. Each quarter, re‑compute your effective rate, scan for new or increased fees, and compare card‑present versus card‑not‑present performance.

Ask your provider to produce a savings report against baseline and to propose optimizations—debit routing improvements, surcharge compliance checks, or Level II/III enablement.

A consistent cadence keeps your credit card processing rates in Erie, Pennsylvania aligned with your goals and forces providers to keep earning your business.

Red flags and bait‑and‑switch warnings

Be careful with quotes that emphasize simplicity without transparency. Tiered pricing labeled “qualified/mid/non‑qualified” often leads to downgrades that inflate your costs. Flat rates can be fine for micro‑ticket merchants, but they hide whether you’re overpaying for regulated debit.

Watch for “free” equipment tied to non‑cancelable leases, auto‑renew contracts, and “program change” clauses allowing unannounced fee increases. If a sales rep refuses to provide an interchange‑plus quote, or declines to model your last three months of Erie sales data, move on.

Beware of extra “regulatory” or “network” fees that duplicate assessments, and of PCI “non‑completion” charges that persist even after you complete validation.

Finally, distrust savings claims that don’t include gateway, POS SaaS, dispute fees, and tokenization costs. A trustworthy provider will put every fee in writing and stand behind a clear, verifiable effective‑rate model.

Frequently Asked Questions

Q.1: What is a “good” effective rate for my Erie business?

Answer: A “good” effective rate depends on your industry, average ticket, card mix, and channel. Quick‑service cafés and convenience retail in Erie, Pennsylvania often target an effective rate under 3% because they run many regulated debit and low tickets where per‑item fees matter most.

Full‑service restaurants with tips and premium rewards cards might land slightly higher due to interchange categories and tip adjustments. B2B distributors using Level II/III data can drive their effective rate down by qualifying for optimized interchange categories, even though their tickets are higher.

The key is not chasing a generic number but benchmarking your current effective rate against a transparent interchange‑plus or membership quote built on your last three months of statements.

If a new offer saves you 30–60 basis points after counting gateway, PCI, POS SaaS, and dispute fees, that’s meaningful. Always evaluate across multiple months to reflect Erie’s seasonality and tourism patterns.

Q.2: Should I choose flat‑rate or interchange‑plus pricing?

Answer: Flat‑rate pricing is simple and predictable, which can help new businesses. But it hides whether you’re overpaying on low‑cost debit and often bundles assessments into a single opaque figure.

Interchange‑plus separates wholesale costs (interchange and assessments) from processor markup so you can compare apples to apples. In Erie, Pennsylvania, where many merchants see a healthy share of debit and seasonal swings, interchange‑plus or membership models typically produce lower long‑term costs, especially as volume grows.

If you prefer flat‑rate for simplicity, ask for written guarantees on no additional monthly fees and confirm how card‑present versus online transactions are priced. No matter the model, compute your effective rate using three months of real statements, including gateway and POS subscription costs, before deciding.

Q.3: Can I legally surcharge credit cards in Pennsylvania?

Answer: You must follow card‑brand rules and Pennsylvania consumer‑protection standards. Credit card surcharges require clear signage, receipt disclosure, and caps; debit and prepaid cannot be surcharged.

Cash discounting and dual pricing are alternatives, but programs must show transparent posted pricing and avoid misrepresenting a “regular” price.

When you compare credit card processing rates in Erie, Pennsylvania, ask providers for state‑specific guidance, sample signage, and POS configuration steps, and verify that fees are removed on PIN debit or other prohibited transactions.

Train staff to explain your policy and to process exceptions gracefully to protect customer goodwill. Because rules and brand bulletins evolve, insist on written compliance support from your provider.

Q.4: How do I negotiate down gateway and POS costs?

Answer: Bundle strategically and ask for caps. Many gateways and POS systems charge per‑transaction fees plus monthly SaaS. If your Erie, Pennsylvania business runs high volume or multiple locations, you can often negotiate lower per‑item fees or volume‑tier discounts.

Ask for tokenization fees to be included in gateway pricing rather than added separately. Seek hardware swap programs and next‑day replacements during peak seasons. If your provider requires annual price escalators, ask for caps tied to CPI with advance notice and a right to terminate without penalty if caps are exceeded.

Always model total cost of ownership—hardware, SaaS, tokenization, and support—against your projected volume to ensure headline rate savings don’t vanish due to platform fees.

Conclusion

Comparing credit card processing rates in Erie, Pennsylvania is about building a full‑picture model of your payment costs and risks, not chasing a catchy discount rate.

Start with a three‑month statement audit, separate interchange and assessments from markup, and insist on transparent interchange‑plus or membership pricing in writing. Model card‑present and online channels separately, then blend them with Erie’s seasonality.

Include gateway, POS SaaS, tokenization, PCI, and dispute costs in your effective‑rate math. Negotiate contract terms that protect your flexibility and avoid long equipment leases.

Finally, set KPIs and review quarterly so your pricing keeps pace with your business and regional patterns. With a structured approach and Erie‑specific considerations in mind, you’ll find a fair, durable plan that lowers your effective rate while supporting fast, secure, and customer‑friendly payments.