Erie’s retail scene—stretching from Peach Street’s big-box corridor to small boutiques along State Street and the Bayfront—has real momentum.

With that momentum comes risk: chargebacks. If you operate a storefront, pop-up, or hybrid eCommerce-plus-brick-and-mortar in Erie, you already know chargebacks can quietly drain profit, erode processor trust, and inflate operating costs.

This guide shows you how to prevent chargebacks in Erie’s retail sector with a practical, step-by-step playbook you can put to work today.

You’ll learn how to harden your policies, tighten checkout, use modern fraud tools, and build a fast dispute-response engine—without making good customers jump through hoops. The goal is fewer disputes, higher recovery rates, and a steady bump in lifetime customer value.

What a Chargeback Really Is—and Why Erie Retailers Feel It More

A chargeback is a forced reversal initiated by the cardholder (or the issuing bank) that pulls funds from your merchant account and sends them back to the customer.

It’s not a refund you control; it’s a network-level clawback with added fees, lost goods, and potential penalties. In practice, chargebacks in Erie’s retail sector usually fall into four buckets:

- Fraudulent/unauthorized transactions. Lost or stolen cards, account takeover, or synthetic identities.

- Customer service disputes. Late delivery, damaged goods, or poor communication.

- Processing errors. Duplicate billing, incorrect amounts, expired authorizations.

- Friendly fraud. A real customer claims non-receipt, dissatisfaction, or “not me” after receiving the item.

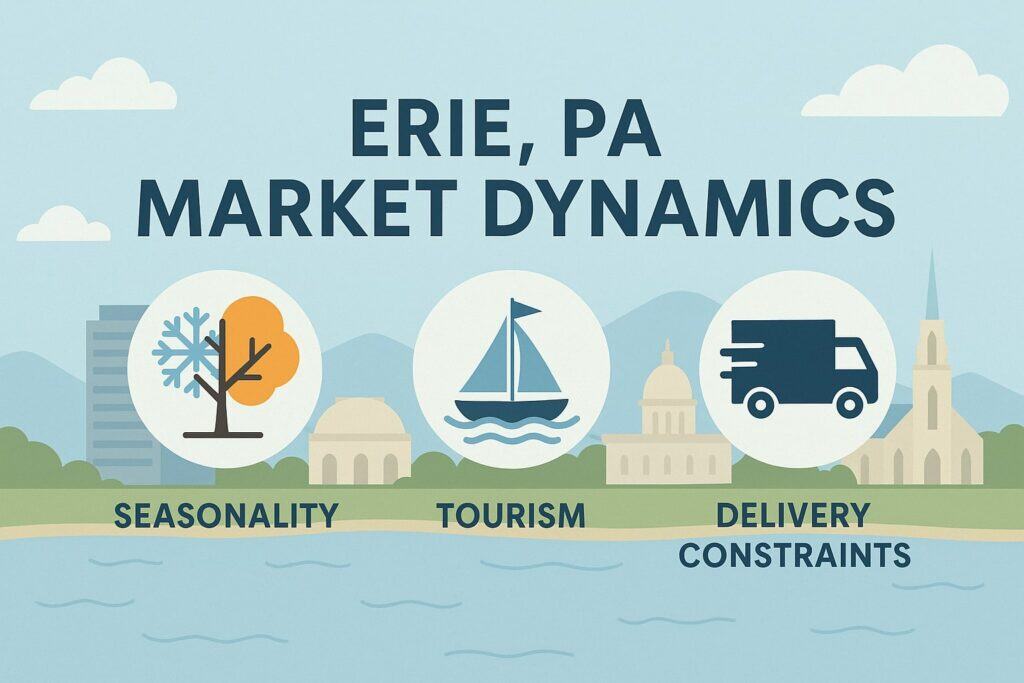

Why do chargebacks in Erie’s retail sector sting more? Local patterns matter. Lake-effect weather affects delivery windows; college calendars drive traffic spikes; summer tourism creates one-time buyers; and events at the Bayfront Convention Center bring national cards that might be more dispute-prone.

Those factors amplify the odds that a normal glitch becomes a chargeback. To prevent chargebacks in Erie’s retail sector, you need layered defenses that reflect these local rhythms—especially around seasonality, staffing, and fulfillment.

Erie, PA Market Dynamics: Seasonality, Tourism, and Delivery Constraints

Erie’s winter can slow carriers and curbside pickup alike, while late spring through early fall fuels visitor traffic along Presque Isle and downtown. That rhythm introduces chargeback risk in three ways:

- Expectation gaps. Tourists expect fast fulfillment and clear pickup directions; locals expect weather-aware ETAs. When reality differs, disputes rise.

- Transient shoppers. One-time buyers are harder to reach post-purchase, making proactive service outreach critical.

- Carrier variability. Winter weather, lake-effect storms, and holiday surges cause delays. Without airtight shipping SLAs and tracking, “item not received” claims spike.

Actionable moves to prevent chargebacks in Erie’s retail sector:

- Publish seasonal shipping cutoffs, pickup hours, and weather advisories on PDPs, checkout pages, and receipts.

- Offer buy online, pick up in store (BOPIS) with photo-verified handoff or PIN-verified pickup to lock in proof of delivery.

- Add SMS status updates for local delivery—especially during storms—so customers don’t jump straight to their bank when an ETA slips.

- For events and festivals, deploy temporary signage and QR-powered help desks (think “Need order help? Scan here”) to intercept problems before they escalate.

Start at the Foundation: Merchant Setup, MCC, and Clean Statement Descriptors

Your merchant account configuration sets the tone for authorization approval, issuer recognition, and dispute routing. To prevent chargebacks in Erie’s retail sector, get the basics right:

- Use the correct MCC (Merchant Category Code). Misaligned MCCs can lead to higher decline rates and more scrutiny from issuers who don’t think your profile fits the purchase.

- Set a clean, human-readable descriptor. Make your billing descriptor match your storefront and domain (e.g., “Erie Gear Co – eriegear.com”). Include a local phone number. Confusing descriptors drive “I don’t recognize this” disputes.

- Enable account updater and network tokenization if your gateway supports them—fewer expired-card issues, smoother recurring payments for subscription-style retail.

- Consistent DBA branding. Align signage, website, receipts, and customer service email so cardholders instantly connect their statement charge with your brand.

These structural steps don’t just reduce confusion; they create issuer familiarity that helps prevent chargebacks in Erie’s retail sector and improves your odds when you fight friendly fraud.

Write Policies That Win Disputes: Refunds, Returns, Exchanges, and Cancellations

Policies are your first line of defense. The right wording (and placement) reduces disputes and powers your representation evidence if a chargeback lands. Build policies to prevent chargebacks in Erie’s retail sector by covering:

- Clear timelines. State exact windows for returns and exchanges (e.g., “30 days from purchase”). In winter, note weather-related extensions for shipments.

- Condition of goods. Define what qualifies for return. Use photos during intake to document conditions—a must for apparel, electronics, and sports gear.

- Refund method and timing. Explain how quickly refunds post (typically 5–10 business days) and how partial refunds work for used/opened items.

- Cancellation rules. For custom orders or special event merchandise, require same-day cancellations or a restocking fee; disclose this at checkout.

- Visible placement. Put policy links in the cart, above the Place Order button, on receipts, and near the POS terminal. Add a short, plain-English summary in store.

When your team follows these rules consistently—and captures buyer consent—you cut “merchandise not as described” and “services not provided” claims, helping prevent chargebacks in Erie’s retail sector all year.

Card-Present (In-Store) Best Practices That Actually Work

If most of your sales are in-store, these POS tactics materially reduce chargebacks:

- Dip or tap—don’t swipe EMV-enabled cards unless absolutely necessary. Improper fallback raises your liability on counterfeit and some fraud claims.

- AVS + ZIP prompts for higher-risk tickets. For large or unusual purchases, politely verify ZIP or ID to deter opportunistic fraud.

- Capture signatures strategically. While not security proof, signatures on high-value items and custom orders add context that helps in representation.

- Receipt discipline. Always print or email itemized receipts. For curbside pickup, note time, associate ID, and include a customer acknowledgment (signature, PIN, or photo).

- Device placement and CCTV. Aim a camera toward your checkout counter. Time-synced footage plus the authorization timestamp is gold when you fight a “card not present” claim on an in-person sale.

Small changes at the terminal level help prevent chargebacks in Erie’s retail sector without slowing the line.

eCommerce and Omnichannel Controls for Erie Retailers

Hybrid merchants—selling online and in store—must synchronize fraud controls across channels. Essentials to prevent chargebacks in Erie’s retail sector online:

- 3-D Secure (3DS) on risky orders. Use adaptive 3DS for high-value, first-time, mismatched AVS/CVV orders to shift liability and block fraud.

- CVV, AVS, and email/phone validation at checkout. Decline or step-up authenticate when data doesn’t align.

- Velocity checks. Flag repeated attempts, abnormal cart values, or multiple cards on one IP/device.

- Geofencing & device fingerprinting. Extra friction when shipping to high-risk ZIPs or when device reputation is poor.

- Order review queue. Lightweight manual review for edge cases near your risk threshold, especially during holiday peaks and Lake-effect storms when deliveries slip.

Tie this to a transparent post-purchase flow—tracking links, SMS alerts, and delivery photos—to stop “item not received” claims before they become chargebacks.

Statement Descriptor, Digital Receipts, and Proactive Notifications

Many disputes start with confusion. Two low-cost steps help prevent chargebacks in Erie’s retail sector:

- Memorable descriptors. Customers should recognize your name in five seconds. Add “ERIE” in the descriptor if your brand name is generic.

- Receipts with context. Email or SMS receipts with store name, address, phone, order summary, pickup instructions, and a one-tap “Need help?” link.

- Post-purchase nudges. Send a short “Everything arrives OK?” message 48–72 hours after delivery. This captures issues before the bank hears about them.

- Subscription reminders. If you run refills or memberships, notify customers before renewals and include an easy cancel path.

These touches build trust and push customers to contact you—not their issuer—cutting preventable chargebacks.

Friendly Fraud Defense and Rock-Solid Representment

Friendly fraud is often a failure of documentation. To prevent chargebacks in Erie’s retail sector and to win the ones that slip through:

- Keep a single “dispute dossier.” Centralize the receipt, order page, product photos, tracking events, delivery proof, signature/PIN, customer emails/SMS, and support logs. Time-stamp everything.

- Use plain language. When you write your rebuttal, be factual and concise: what was sold, when it shipped, how it was delivered, and evidence of use/receipt.

- Match the reason code. Tailor your evidence to “not received,” “not as described,” or “fraudulent”—don’t send a catch-all packet.

- Refund when it’s right. If you’re clearly at fault, refund fast and document it. Quick resolutions reduce repeat disputes and bad reviews.

Over time, a crisp representation process deters serial abusers and helps prevent chargebacks in Erie’s retail sector by setting expectations that claims will be challenged with evidence.

Train Your Team: Scripts, Checklists, and Ownership

Humans beat chargebacks when they have structure. Build a short playbook:

- Greeting and checkout scripts to verify identity politely on high-risk tickets (“Would you mind confirming the billing ZIP on your card?”).

- Pickup checklist for BOPIS: verify order ID, match name to ID, take a handoff photo (product + customer), and time-stamp the exchange.

- Return intake protocol with condition photos and reason codes that map to your POS.

- Escalation matrix for suspicious behavior, card declines, or mismatched AVS/CVV in eCommerce.

Celebrate save-stories at team meetings. When staff know how they help prevent chargebacks in Erie’s retail sector, they’ll engage more, spot red flags faster, and protect margins.

Inventory, Fulfillment, and Delivery Proofs—Make “INR” Hard to Claim

“Item Not Received” drives a disproportionate share of disputes. To prevent chargebacks in Erie’s retail sector on this front:

- Package photos and weight capture. Photograph sealed boxes and log actual weight; this rebuts empty-box claims.

- Signature or PIN for high-value goods. Configure carriers for signature on delivery over a threshold (you choose the cutoff).

- Locker pickup or in-store handoff for risky addresses; require photo ID.

- GPS-stamped delivery photos for local delivery—porch shot with door, package, and recognizable feature (doormats, house number).

- Clear returns logistics. Include a prepaid label for eligible returns and spell out the condition requirements.

These low-friction controls measurably reduce chargebacks tied to fulfillment.

Fraud Tools That Actually Move the Needle

Technology helps prevent chargebacks in Erie’s retail sector without punishing good buyers:

- Gateway-level rules. AVS/CVV enforcement, velocity limits, and blacklists/whitelists.

- Risk scoring. Use machine-learned signals (device, IP, BIN, behavioral data) to approve, review, or decline.

- 3-D Secure with exemptions. Apply 3DS selectively to shift liability while preserving conversion.

- BIN intelligence. Handle prepaid/gift cards more carefully; require signature or pickup verification.

- Chargeback alerts and deflection. Some services notify you before a dispute formalizes, letting you refund or contact the buyer proactively.

Combine automation with a quick manual review for edge cases. This hybrid model keeps acceptance high while you prevent chargebacks.

Measure What Matters: KPIs, Dashboards, and Thresholds

You can’t prevent chargebacks in Erie’s retail sector without visibility. Track:

- Chargeback rate (count-based and dollar-weighted) by channel and product.

- Dispute reason codes and win rate by category (INR, not as described, fraud).

- Time-to-first-response on disputes and average representation cycle days.

- Refund ratio vs. disputes. Proactive refunds that prevent escalation are a win when you’re at fault.

- Authorization approval rate and false-decline rate—overly strict rules can backfire.

Set monthly thresholds (e.g., “chargeback rate < 0.7%,” “representation win rate > 60%”). When a metric slips, trigger your crisis playbook.

Working With Issuers, Acquirers, and the Card Brands

Partnerships help you prevent chargebacks in Erie’s retail sector:

- Talk to your processor. Ask for reason-code analytics and network best practices relevant to your vertical.

- BIN and issuer insights. Identify banks that drive a disproportionate share of disputes and adjust your step-up rules for their cards.

- Compliance reviews. Keep descriptors, refund timelines, and disclosure placement up to network expectations.

When banks see you respond quickly with strong evidence, they recognize you as a low-risk merchant—raising your long-term authorization approvals and lowering scrutiny.

Compliance and Practical Legal Hygiene (Plain-English)

This isn’t legal advice, but practical hygiene matters to prevent chargebacks in Erie’s retail sector:

- PCI DSS. Keep POS devices patched, limit who sees card data, and use tokenization. Train staff to spot skimmers and tampering.

- Surcharging & fees. If you add convenience fees or surcharges, disclose clearly and follow network rules and local requirements. Transparency reduces post-purchase friction.

- Sales tax clarity. Show tax line items before payment. Confusion over totals often leads to “incorrect amount” disputes.

- Privacy and consent. For SMS and email, secure opt-in. Consent records support your contact outreach when resolving disputes.

Clear, visible disclosures lower the odds that a customer feels misled and heads straight to their bank.

When Chargebacks Spike: A 7-Day Crisis Playbook

If your chargebacks surge—holiday rush, a bad batch of inventory, or a courier outage—move fast:

Day 1–2: Stabilize

- Tighten fraud rules temporarily (enable 3DS for more traffic, raise review thresholds).

- Post shipping advisories and extend return windows if weather is impacting deliveries.

Day 3–4: Contain

- Email/SMS recent buyers with updated ETAs and support links.

- Offer fast refunds where you know you’re at fault; it’s cheaper than a dispute.

Day 5–6: Investigate

- Segment disputes by reason code and product SKU. Pull camera footage for in-store anomalies. Review carrier scans and handoff logs.

Day 7: Reset

- Roll back any over-tight rules that hurt conversion.

- Update FAQs, policy language, and training scripts based on what you learned.

Executing quickly can prevent chargebacks in Erie’s retail sector from triggering network monitoring programs or higher processing costs.

Product and Pricing Triggers You Might Be Missing

Some SKUs attract chargebacks: electronics, collectibles, pre-orders, custom items, and seasonal apparel. To reduce risk:

- For pre-orders, state the expected ship date and auto-update customers monthly until it ships.

- For custom goods, collect design approvals in writing, with mockups and final sign-off.

- For high-value items, require signature and ID verification at pickup.

Price transparency matters too. Break out add-ons, warranties, and assembly fees clearly at checkout and on the receipt. Surprises create disputes.

Local Touches That Win in Erie

Lean into your local edge to prevent chargebacks in Erie’s retail sector:

- Local phone support. A recognizable 814 number reduces to “who is this?” panic when a customer checks their statement.

- Weather-smart ETAs. Post “Lake-effect delays possible” messaging with realistic windows during storm forecasts.

- Community presence. Prominent social profiles and Google Business updates make your brand feel reachable; reachable brands get emails, not disputes.

These small, Erie-specific cues build trust and lower chargeback propensity.

Technology Checklist: Your 12-Point Anti-Chargeback Stack

- Clean descriptor with local phone number

- AVS/CVV enforcement and flexible risk rules

- Adaptive 3-D Secure for high-risk orders

- Velocity checks on cards, IPs, and devices

- Device fingerprinting and geolocation filters

- Manual review queue for edge cases

- Digital receipts with one-tap support

- BOPIS handoff logging with photo/PIN

- Signature on delivery for high-value shipments

- Chargeback alerts/deflection where available

- Centralized dispute dossier builder

- KPI dashboard with monthly thresholds

Implementing this stack helps prevent chargebacks in Erie’s retail sector while keeping checkout smooth.

FAQs

Q1: What’s the fastest way to prevent chargebacks in Erie’s retail sector before the holidays?

Answer: Enable adaptive 3-D Secure for first-time, high-ticket, or mismatched AVS/CVV orders; require signature on delivery over a set threshold; and publish clear cutoffs and weather advisories on product pages and at checkout. Add proactive SMS updates for pending deliveries so customers contact you first, not their bank.

Q2: Should I refund or fight a dispute?

Answer: Refund quickly when you’re clearly at fault (late shipment without communication, wrong item with proof). Fight when you have strong proof of delivery or usage (BOPIS handoff, delivery photo with GPS, signed pickup, support emails acknowledging receipt). Over time, a consistent stance deters friendly fraud.

Q3: Do signatures still matter in-store?

Answer: They’re not a silver bullet, but for high-value items and custom work, a signature plus EMV or contactless authentication adds context. Pair it with CCTV timestamps and a detailed receipt to strengthen your representation packet.

Q4: How do I reduce “I don’t recognize this” disputes?

Answer: Use a plain-English descriptor matching your storefront and website, include “ERIE” if your brand name is generic, and attach a local phone number. Send itemized digital receipts with a “Need help?” link. These steps alone can noticeably prevent chargebacks.

Q5: Are prepaid and gift cards riskier?

Answer: Often. Set lower approval thresholds, require ID on in-store pickup, and consider 3DS or manual review for large eCommerce orders on prepaid BINs. This protects against resellers and synthetic identities.

Q6: What reports should I review monthly?

Answer: Chargeback rate by reason code, win rate, SKU-level dispute incidence, authorization approvals, false declines, and time-to-first-response. Use a dashboard that flashes red when thresholds are breached so you can act before a network program triggers.

Q7: How can weather-related delays avoid becoming disputes?

Answer: Over-communicate. Post seasonal advisories, send ETA updates, and offer easy returns or partial credits when delays exceed expectations. Communication converts potential chargebacks into loyalty moments.

Conclusion

To prevent chargebacks in Erie’s retail sector, think layers, not silver bullets. Start with fundamentals—accurate MCC, clean billing descriptors, and crystal-clear policies. Add practical POS discipline in store and smart risk controls online.

Build a proactive service loop with receipts, SMS updates, and weather-aware ETAs. Then, prepare a lean, evidence-rich representation workflow for the few disputes that still occur. Back everything with simple KPIs and a 7-day crisis plan.

When you combine Erie-specific touches—local phone support, seasonal messaging, and community presence—with modern risk tools and disciplined operations, you’ll see fewer disputes, faster resolutions, and healthier margins.

That’s how you sustainably prevent chargebacks in Erie’s retail sector while keeping checkout smooth and customers happy.